This post about the future of Venture Capital and ICOs (Initial Coin Offerings) is an excerpt from the full article, found here at toptal.com. I focused on the Machine Learning and human talent aspects and how they will impact the future of the industry. Another post of interest about the future of the crowdfunding market can be found here.

-Spencer

BY ALEX GRAHAM – FINANCE EXPERT @ TOPTAL (original article posted here)

Executive Summary

Is the VC industry at a crossroads?

- Returns from venture capital continue to underperform both private equity and public markets. Cambridge Associates’ current 10-year return for VC is approximately 15%, which is below the generally accepted par of 20% for the asset class.

- The median time to exit via IPO for venture-backed startups is now 8.2 years, and the slow pace of exits is affecting managers’ abilities to generate returns and pay back investors.

- A series of scandals in 2017 dented the public image of venture capital firms and exposed malpractice in the industry that could be detrimental to investment performance.

- VCs face enhanced competition from other investors to find the best startup deals. In June 2017, investing in ICOs surpassed VC investing, and in the US, corporates now account for a quarter of all startup financing.

What are the root causes of problems in the VC industry?

- Information about investing in startups used to be hard to access, but recent advances in technology have democratized this and allowed other investors to compete with VC funds.

- The ten-year life of a VC fund is being tested by longer waits to exit for individual investments. In addition, as VC funds have gotten larger, GPs’ increased allocation of management fees may be distorting the incentive structures of the asset class.

- With VC investment comes pressure and oversight. Many entrepreneurs now are looking for easier investment options from ICO token raises and other passive investors.

How can the future of venture capital shape up?

- VC funds should look to deploy big data techniques to help them parse more deal flow information and get to the best deals quicker. Finding the best talent even earlier will help them to get to the front of the queue

- To alleviate fund life expectancy, more exotic fund structures such as evergreen funding and pledge funds would afford more flexibility to investment managers and align goals with LPs.

- The practice of offering platform services to portfolio companies is a key differentiator for VC funds. It is, however, an expensive service, and smaller funds should look to cast a wider net within the entire entrepreneurship ecosystem, use virtual advisors more, and try to enhance interdependence amongst portfolio companies better.

How Can the Future of Venture Capital Shape Up?

VCs Need to Get to the Front of the Next Information Advantage

Despite increased access to information, the best funds and venture analysts will still retain the intangible skills of being able to parse wide swathes of information and find the best deals. One way that the VC fund of the future could stand out, get to the front of the queue on deals, and be efficient cost-wise would be to use big data to greater effect. This is something that may be scoffed at by purists, but a tandem approach of quantitative with qualitative decision making would allow funds to spot leading indicators quicker and mitigate biases.

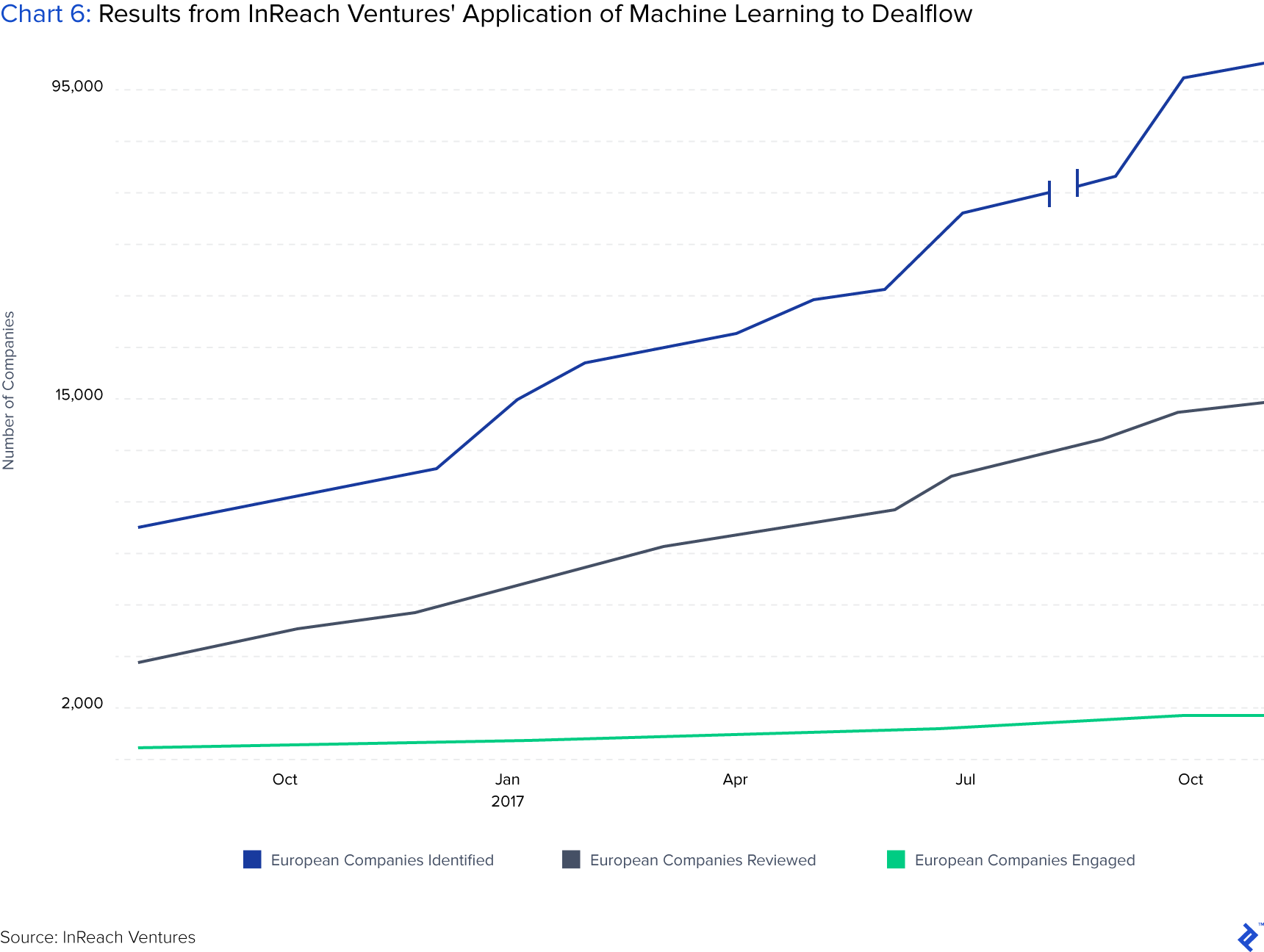

Chart 6 below shows what InReach Ventures achieved using proprietary machine learning tools to build dealflow in Europe. Within a year, it collated over 95,000 companies, of which 15,000 were reviewed and then 2,000 engaged with. It also allowed them to spot a hidden gem called Oberlo, which was later acquired by Shopify.

Arguments against this would cry “this is a quantity over quality approach!” But I think this displays an interesting angle to overcoming behavioral biases and showing how the VC industry could scale.

Social Capital has tested an initiative it calls “capital as a service,” which aims to automate the investment pitch and decision process. Startups apply online and go through selection steps without any human intervention. Its initial results showed some interesting contrarian trends that give credence towards giving all startups a level playing field with an objective non-human filter:

“In our pilot, we evaluated nearly 3,000 companies and committed to funding several dozen of those, across 12 countries and many sectors, without a single traditional venture pitch. In fact, in most cases, the data-driven approach allowed us to reach conviction around an investment opportunity before we ever even spoke to the founders.”

If Investing in Talent Is Key, Then Find It Earlier

The earlier that you spot and invest in a startup with potential, the better. Historically, that would constitute making a set of small seed investments, then following on the winners in later rounds. Yet as investment rounds have gotten bigger, the concept of “historic seed” has become Series A, and now pre-seed is seen as the path to being the first institutional check in a company.

Being the first check is one of the best differentiators that an active VC investor can take to stand out and outperform newer, less experienced investors. One way that VCs can take this even further is to go back even earlier, before the pre-seed round… to before the startup has even been born.

Finding inspirational talent that does not yet have an idea could be one part of the future of venture capital. Taking an equity stake in their “future idea” would be a way to encourage raw talent to go away with the backing some financial resources and see what they come up with.

Human talent is regularly seen as the core ingredient of success in a startup, superseding the business idea. A Gallup study claimed that highly talented entrepreneurs outperform their peers in year-on-year profit growth by 22%. Finding and connecting talent does not go unnoticed, VC Mark Suster defines his job as being the “chief psychologist” and claims that:

“We’re supposed to be good judges about which entrepreneurs and executives have both the most clever ideas and the right skill sets to do transformational things against all odds.”

Company builders have followed this style to an extent, but the great talent that they have are never the “true” owners of their business because they are salaried employees with reduced equity ownership. Spotting talent is what VCs do best, and they should go to the habitat of talent and get in their ear before they even have an idea.

Get Leaner, Go Earlier, and Get Focused

Despite middling returns, venture capital remains a glamorous industry. For many, it offers the intersection of financial dealmaking with the ability to make tangible and positive interventions post investment.

The growth in popularity of the VC industry has seen new funding competition emerge and behavioral preferences change, which can be incongruous to the traditional model of venture capital. I’m not saying that the industry is going to die out at all—instead, just making a case that certain changes could be made to ensure that LPs get a good deal and VCs deploy their talents in an optimal way.

My vision of the future for the “rest of the pack” is that a combination of the following will occur:

- Machines will take over half of the role that associates currently perform.

- New funds will have to go back even earlier in the lifecycle to find companies.

- Generalist investment theses will only be reserved for proven “home run” funds or growth equity-focused ones.

- The closed-end legal model will evolve into structures that align timing and incentives better.

The emergence of ICOs could act as the catalyst for this change, and I for one hope that VC retains its relevance. What makes now an important time to act is that the fortunes of VC will be tied to the ICO market and, through a misconception of association, VCs will be tarred with the same brush of any scandals that arise from them.

UNDERSTANDING THE BASICS

What is venture capital and how does it work?

Venture capital is equity financing provided to high-risk companies with high growth potential. The goal of a VC is to realize a return by selling their shares when the company lists on a stock exchange or is bought by another.

What is an ICO?

An initial coin offering (ICO) is a fundraising issuance of tokens that functions as a currency within the issuer’s blockchain project. The behavior of these tokens functions similarly to shares in that they reflect the underlying fortunes of the business.

What is an IPO exit strategy?

Planning to exit via IPO means a business has an end plan of issuing its stock on the public markets and providing its private backers with a liquid market with which to sell their equity to public market investors.

What is the difference between angel investors and venture capitalists?

Angel investors are typically private individuals that invest their wealth into startups at the early stage of their lives. While venture capitalists also invest in such companies and stages, their source of capital is generally not their own. They act as investment managers for other investors, known as LPs.

About the author

Alex is a London-based CFA who has had a career across the world. He enjoys freelancing to keep abreast of industry trends and to reinforce his experience from venture capital, consulting and bond/currency trading. With a technical skill set and an engaging communicative touch, he is proficient at valuations and market analysis. His breadth of work has ranged from projects with the Bank of England to helping a jewelry entrepreneur to fundraise.